close

Choose Your Site

Global

Social Media

Views: 7 Author: Site Editor Publish Time: 2018-11-11 Origin: Site

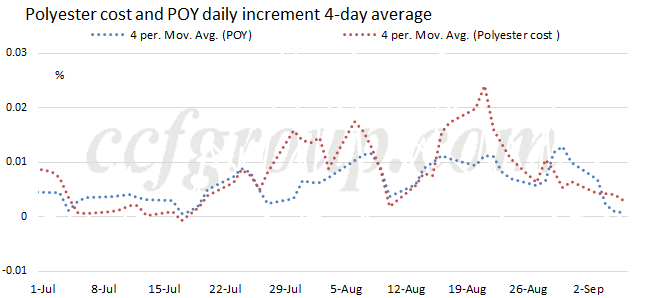

Polyester filament yarn plants witnessed rapidly rising melt cost but hard-to-rise downstream sectors in Aug, and the monthly sales ratio was only around 100%. Coupled with the pre-sales in PFY plants even without stocks at hand, cash flow of PFY was substantially squeezed in Aug, and FDY were not profitable

| Cash flow of PFY in Aug 2018 (Unit: yuan/mt) | ||

| POY150D/48F | FDY150D/96F | |

| Average price in Aug | 11,166 | 11,071 |

| Cash flow (Based on domestic average price) | 499 | 4 |

| Cash flow (Based on settlement price) | 388 | -107 |

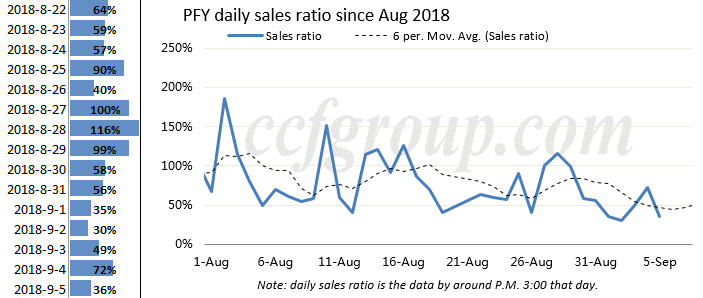

Entering Sep, sales ratio of PFY kept weakening and was mainly around 30-40% in recent days.

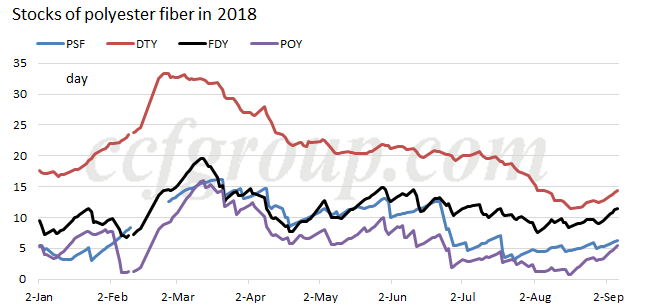

Thus, inventory of PFY accumulated rapidly.

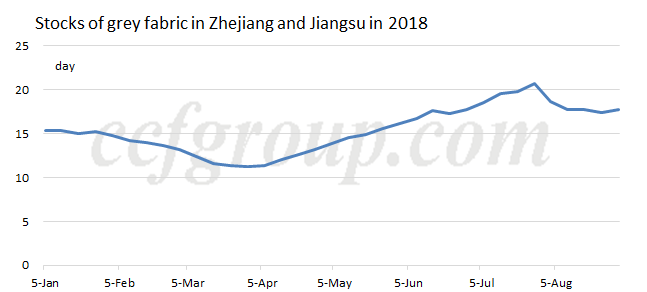

As for downstream weaving market, the upward potential of PFY dwindles now, favoring the cost lock-in for new orders, but new orders for grey fabric have big discussion pressure under high-priced feedstock cost. Thus, weaving plants still meet difficulty in placing orders. In addition, some PFY plants discount offers when the uptrend of melt cost and PFY price stagnates, so many downstream purchasers show stronger sidelined mindset. Inventory of grey fabric remains high despite of the reduction of loom run rate.

Some downstream plants slash run rate to control the increases of inventory, dragging down demand for PFY, so inventory of PFY is expected to rise further. Coupled with the speculative inventory accumulated in Aug, downstream players do not lack feedstock, providing their confidence to watch and see for a period.

Besides, export of PFY and its downstream products is expected to be stunted with exchange rate risk, the tariff addition of US and high-priced domestic PFY price.

Supply/demand pressure still exist on PTA market in Sep. Some polyester plants scale down production and turn to sell PTA under high price recently, but mainstream suppliers are firm in selling spot PTA high. Some PTA plants are scheduled to have turnaround in the future, so polyester feedstock market may sustain high. However, the turnaround may be delayed with high PX-PTA spread, and combined with falling buying interest, feedstock market is likely to head south.

Cash flow of polyester products remains low with strong melt cost. Mainstream products including FDY, DTY, PET fiber chip, PET bottle chip and PSF were not profitable in early-Sep, except for POY with minor profit. In short run, PFY plants are expected to see moderate inventory burden, and PFY price is supposed to remain high and firm, not ruling out the price cut in some plants based on inventory and capital status.

| Cash flow of polyester products since Sep 2018 | ||||||

| Unit: yuan/mt | PET fiber chip | POY150/48 | FDY150/96 | DTY150/48 | PET bottle chip | PSF |

| 2018-9-6 | -111.15 | 458.85 | -61.15 | -100 | -261.15 | -181.15 |

| 2018-9-5 | -106.88 | 473.13 | -56.88 | -110 | -256.88 | -166.88 |

| 2018-9-4 | -91.8 | 473.2 | -56.8 | -95 | -191.8 | -151.8 |

| 2018-9-3 | -168.48 | 451.52 | -83.48 | -75 | -318.48 | -153.48 |

| 2018-8-31 | -60.22 | 549.78 | 24.78 | -65 | -435.22 | -80.22 |

In medium run, downstream sectors can choose to avoid high-priced products to a certain extent by suspending production temporarily when the cost of production stop is not high. The cost for PFY plants suspending production is relatively higher. Inventory of PFY is anticipated to mount in Sep, and the feedstock cost is largely high. Once feedstock market turns to decrease, the stagnated inventory is expected to face bigger devaluation burden.